# backtrader_next

**Repository Path**: jiaping/backtrader_next

## Basic Information

- **Project Name**: backtrader_next

- **Description**: backtrader_next镜像

- **Primary Language**: Unknown

- **License**: GPL-3.0

- **Default Branch**: master

- **Homepage**: None

- **GVP Project**: No

## Statistics

- **Stars**: 0

- **Forks**: 0

- **Created**: 2026-03-22

- **Last Updated**: 2026-03-22

## Categories & Tags

**Categories**: Uncategorized

**Tags**: None

## README

# backtrader-next

[](https://pypi.org/project/backtrader_next/)

[](https://pypistats.org/packages/backtrader_next)

[](https://python.org "Go to Python homepage")

[](https://github.com/smalinin/backtrader_next/blob/master/LICENSE)

Live Trading and backtesting platform written in Python.

## Installation

```

pip install backtrader-next

```

## History

Package is based on [backtrader](https://github.com/mementum/backtrader)

Changes:

- Added new Chart plotting using bn-lightweight-charts-python.

- Improved testing performance by using the `PandasData` feed in `runonce=True` mode.

- Added performance statistics in both text format (similar to Backtesting.py) and HTML format (similar to Quantstats).

- Improved support for switching between futures (for testing, etc.).

- Added new indicators implemented with Numba.

- Improved performance — now it runs about 2–3× slower than Backtesting.py in `runonce=True` mode with `PandasData`.

- Detailed results

- Interactive visualizations

## Performance

Performance comparison using the [perf_compare](https://github.com/smalinin/backtrader_next/tree/master/examples/3_perf_compare) benchmark.

- **Backtrader-next** using an optimized **PandasData** feed

- [Backtrader](https://github.com/mementum/backtrader) with **PandasData** feed

- [Backtesting.py](https://github.com/kernc/backtesting.py)

| Framework | Execution Time | Relative Speed |

|---|---|---|

| Backtesting | 2.95 sec | 14.3x faster than Backtrader |

| Backtrader-next | 12.33 sec | 3.4x faster than Backtrader |

| Backtrader | 42.25 sec | Baseline |

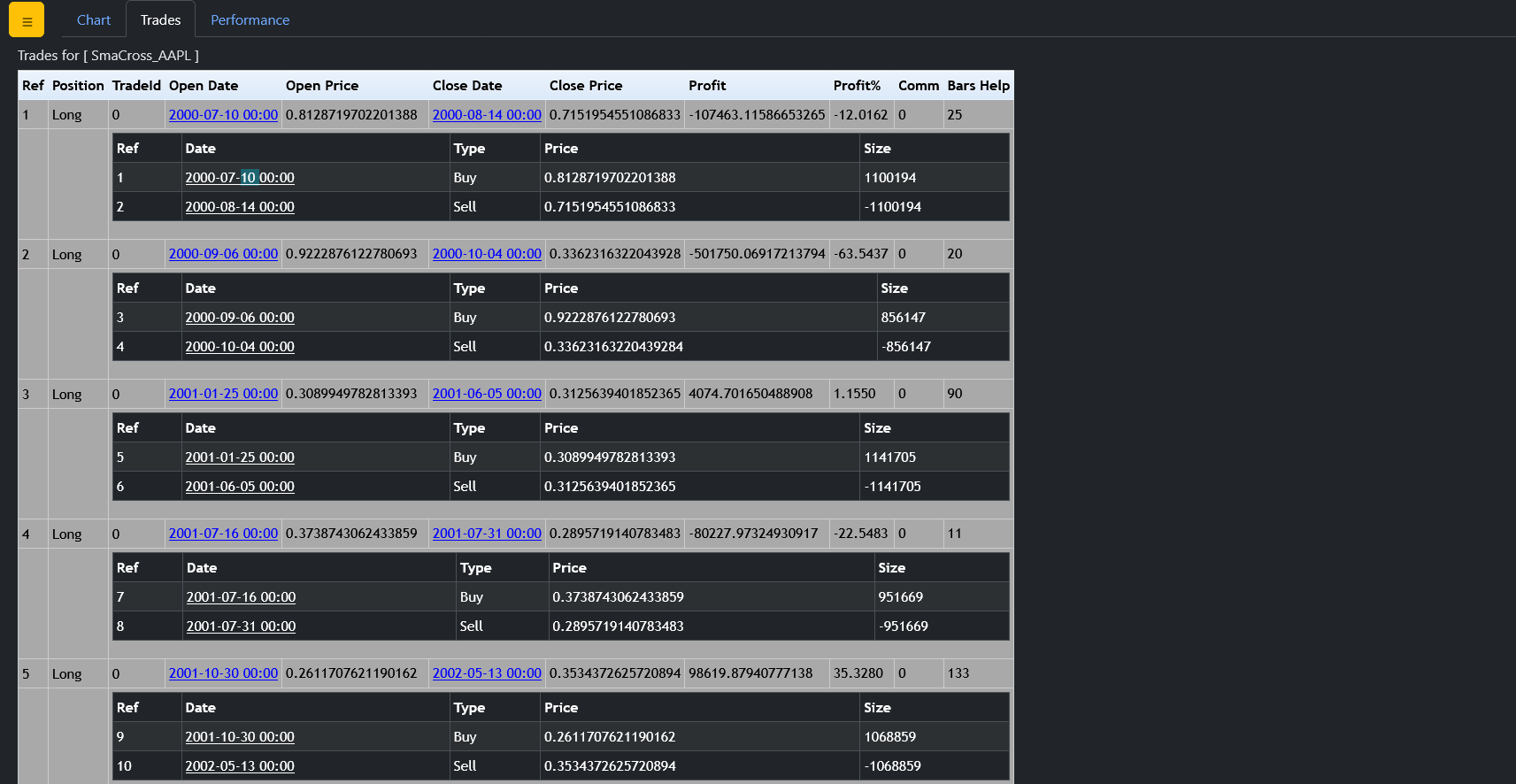

## Here a snippet of a Simple Moving Average CrossOver.

```python

import pandas as pd

import backtrader_next as bt

from backtrader_next.feeds import PandasData

class SimpleSizer(bt.Sizer):

params = (

('percents', 99),

)

def _getsizing(self, comminfo, cash, data, isbuy):

value = self.broker.getvalue()

price = data.close[0]+comminfo.p.commission

size = value / price * (self.p.percents / 100)

return int(size)

class SmaCross(bt.Strategy):

params = (

('MA1', 20),

('MA2', 50),

)

def __init__(self):

self.Order = None

self.ma1 = bt.nind.SMA(self.data.close, period=self.p.MA1)

self.ma2 = bt.nind.SMA(self.data.close, period=self.p.MA2)

def notify_order(self, order):

if order.status in [order.Submitted, order.Accepted]: # Order is submitted/accepted

return # Do nothing until the order is completed

# if order.status in [order.Completed]: # Order is completed

# if order.isbuy(): # Buy order

# pass

# elif order.issell(): # Sell order

# pass

elif order.status in [order.Canceled]: # Canceled, Margin, Rejected

print('Order was Canceled', self.data.datetime.datetime(0))

elif order.status in [order.Margin]: # Canceled, Margin, Rejected

print('Order was Margin ', self.data.datetime.datetime(0))

elif order.status in [order.Rejected]: # Canceled, Margin, Rejected

print('Order was Rejected', self.data.datetime.datetime(0))

self.Order = None # Reset order

def next(self):

# Use ONLY Long Positions

if self.crossover(self.ma1, self.ma2):

pos = self.getposition()

if pos:

self.close(size=pos.size)

self.Order = self.buy()

elif self.crossover(self.ma2, self.ma1):

pos = self.getposition()

if pos:

self.close(size=pos.size)

# self.Order = self.sell()

def crossover(self, ma1, ma2):

try:

return ma1[-1] <= ma2[-1] and ma1[0] > ma2[0]

except IndexError:

return False

if __name__ == '__main__':

cerebro = bt.Cerebro()

cerebro.broker.setcash(1_000_000.0)

cerebro.broker.set_shortcash(False)

cerebro.broker.setcommission(commission=0, margin=False)

cerebro.addsizer(SimpleSizer, percents=90)

df = pd.read_csv(f"AAPL_1d.csv.zip", sep=";")

df['Datetime'] = pd.to_datetime(df['Date'].astype(str) , format='%Y-%m-%d')

df.set_index('Datetime', inplace=True)

data = PandasData(dataframe=df, timeframe=bt.TimeFrame.Days, compression=1)

cerebro.adddata(data, name='AAPL')

cerebro.addstrategy(SmaCross, )

print(f'Starting Portfolio Value: {cerebro.broker.getvalue():.2f}\n')

results = cerebro.run()

print(f'\nFinal Portfolio Value: {cerebro.broker.getvalue():.2f}\n')

rc = cerebro.statistics

print(rc)

# old plot required matplotlib

# cerebro.old_plot(style='candle')

cerebro.plot(filename="smacross.html")

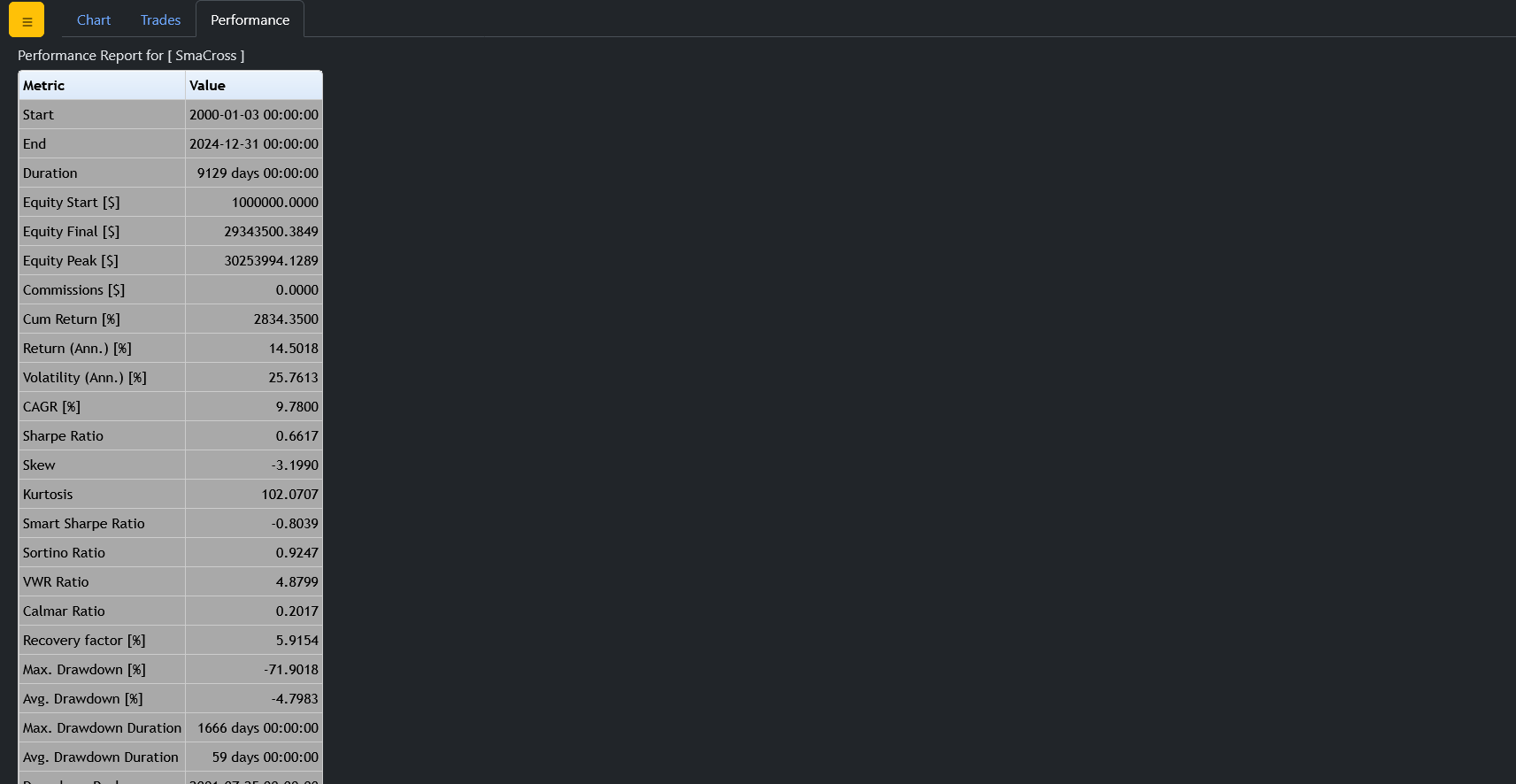

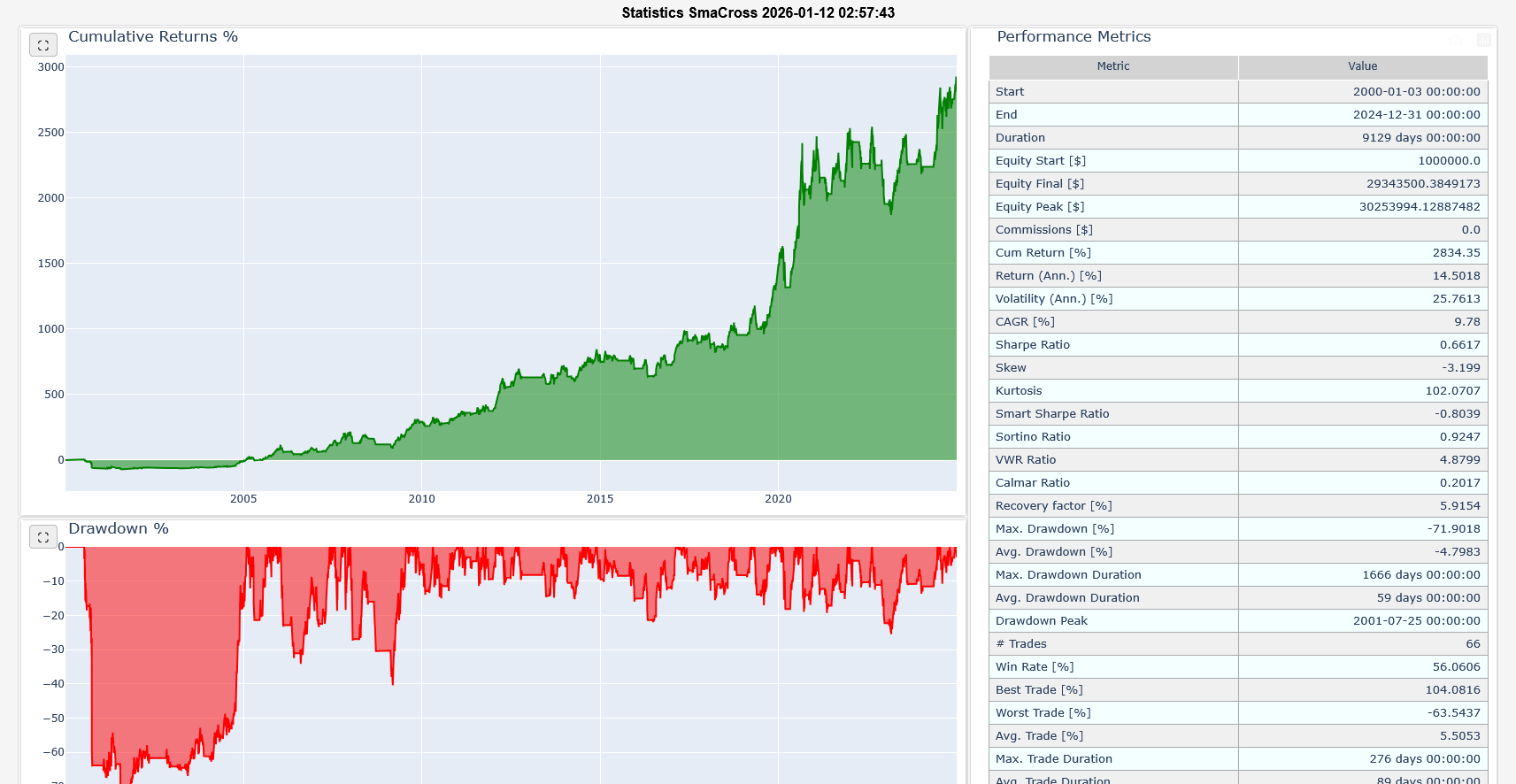

cerebro.show_report(filename="smacross_stats.html")

print("end")

```

#### Output log

```

Starting Portfolio Value: 1000000.00

Final Portfolio Value: 29343500.38

Strategy SmaCross

MA1 20

MA2 50

Start 2000-01-03 00:00:00

End 2024-12-31 00:00:00

Duration 9129 days 00:00:00

Equity Start [$] 1000000.0

Equity Final [$] 29343500.384917

Equity Peak [$] 30253994.128875

Commissions [$] 0.0

Cum Return [%] 2834.35

Return (Ann.) [%] 14.5018

Volatility (Ann.) [%] 25.7613

CAGR [%] 9.78

Sharpe Ratio 0.6617

Skew -3.199

Kurtosis 102.0707

Smart Sharpe Ratio -0.8039

Sortino Ratio 0.9247

VWR Ratio 4.8799

Calmar Ratio 0.2017

Recovery factor [%] 5.9154

Max. Drawdown [%] -71.9018

Avg. Drawdown [%] -4.7983

Max. Drawdown Duration 1666 days 00:00:00

Avg. Drawdown Duration 59 days 00:00:00

Drawdown Peak 2001-07-25 00:00:00

# Trades 66

Win Rate [%] 56.0606

Best Trade [%] 104.0816

Worst Trade [%] -63.5437

Avg. Trade [%] 5.5053

Max. Trade Duration 276 days 00:00:00

Avg. Trade Duration 89 days 00:00:00

Profit Factor 1.1704

Expectancy [%] 0.0676

SQN 2.4064

Kelly Criterion [%] 39.2016

dtype: object

end

```

It will create two HTML files and open it in your current browser.

- [smacross.html](https://smalinin.github.io/backtrader_next/1_smacross/smacross.html) - charts and trade stats

- [smacross_stats.html](https://smalinin.github.io/backtrader_next/1_smacross/smacross_stats.html) - quantstats like strategy report

## Features:

Live Trading and backtesting platform written in Python.

- Live Data Feed and Trading with

- Interactive Brokers (needs ``IbPy`` and benefits greatly from an

installed ``pytz``)

- *Visual Chart* (needs a fork of ``comtypes`` until a pull request is

integrated in the release and benefits from ``pytz``)

- *Oanda* (needs ``oandapy``) (REST API Only - v20 did not support

streaming when implemented)

- Data feeds from csv/files, online sources or from *pandas* and *blaze*

- Filters for datas, like breaking a daily bar into chunks to simulate

intraday or working with Renko bricks

- Multiple data feeds and multiple strategies supported

- Multiple timeframes at once

- Integrated Resampling and Replaying

- Step by Step backtesting or at once (except in the evaluation of the Strategy)

- Integrated battery of indicators

- *TA-Lib* indicator support (needs python *ta-lib* / check the docs)

- Easy development of custom indicators

- Analyzers (for example: TimeReturn, Sharpe Ratio, SQN) and ``pyfolio``

integration (**deprecated**)

- Flexible definition of commission schemes

- Integrated broker simulation with *Market*, *Close*, *Limit*, *Stop*,

*StopLimit*, *StopTrail*, *StopTrailLimit*and *OCO* orders, bracket order,

slippage, volume filling strategies and continuous cash adjustmet for

future-like instruments

- Sizers for automated staking

- Cheat-on-Close and Cheat-on-Open modes

- Schedulers

- Trading Calendars

- Plotting (requires matplotlib)

## Documentation

The old blog for backtrader:

- `Blog `_

Read the full old documentation at:

- `Documentation `_

List of built-in Indicators (122)

- `Indicators Reference `_

An example for *IB* Data Feeds/Trading:

- ``IbPy`` doesn't seem to be in PyPi. Do either::

pip install git+https://github.com/blampe/IbPy.git

or (if ``git`` is not available in your system)::

pip install https://github.com/blampe/IbPy/archive/master.zip

For other functionalities like: ``Visual Chart``, ``Oanda``, ``TA-Lib``, check

the dependencies in the documentation.

From source:

- Place the *backtrader_next* directory found in the sources inside your project

Version numbering

=================

X.Y.Z

- X: Major version number. Should stay stable unless something big is changed

like an overhaul to use ``numpy``

- Y: Minor version number. To be changed upon adding a complete new feature or

(god forbids) an incompatible API change.

- Z: Revision version number. To be changed for documentation updates, small

changes, small bug fixes