# FinRL-Library

**Repository Path**: zhangzihan/FinRL-Library

## Basic Information

- **Project Name**: FinRL-Library

- **Description**: No description available

- **Primary Language**: Unknown

- **License**: MIT

- **Default Branch**: master

- **Homepage**: None

- **GVP Project**: No

## Statistics

- **Stars**: 0

- **Forks**: 1

- **Created**: 2021-03-15

- **Last Updated**: 2021-03-15

## Categories & Tags

**Categories**: Uncategorized

**Tags**: None

## README

# FinRL: A Deep Reinforcement Learning Library for Quantitative Finance [![twitter][1.1]][1] [![facebook][1.2]][2] [![google+][1.3]][3] [![linkedin][1.4]][4]

[1.1]: http://www.tensorlet.com/wp-content/uploads/2021/01/button_twitter_22x22.png

[1.2]: http://www.tensorlet.com/wp-content/uploads/2021/01/facebook-button_22x22.png

[1.3]: http://www.tensorlet.com/wp-content/uploads/2021/01/button_google_22.xx_.png

[1.4]: http://www.tensorlet.com/wp-content/uploads/2021/01/button_linkedin_22x22.png

[1]: https://twitter.com/intent/tweet?text=FinRL-A-Deep-Reinforcement-Learning-Library-for-Quantitative-Finance%20&url=hhttps://github.com/AI4Finance-LLC/FinRL-Library&hashtags=DRL&hashtags=AI

[2]: https://www.facebook.com/sharer.php?u=http%3A%2F%2Fgithub.com%2FAI4Finance-LLC%2FFinRL-Library

[3]: https://plus.google.com/share?url=https://github.com/AI4Finance-LLC/FinRL-Library

[4]: https://www.linkedin.com/sharing/share-offsite/?url=http%3A%2F%2Fgithub.com%2FAI4Finance-LLC%2FFinRL-Library

[](https://pepy.tech/project/finrl)

[](https://pepy.tech/project/finrl)

[](https://www.python.org/downloads/release/python-360/)

[](https://pypi.org/project/finrl/)

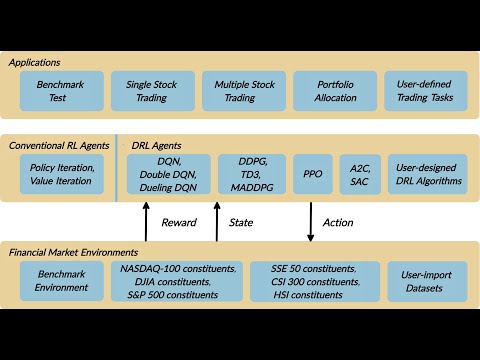

FinRL is an open source library that provides practitioners a unified framework for pipeline strategy development. **In reinforcement learning (or Deep RL), an agent learns by continuously interacting with an environment, in a trial-and-error manner, making sequential decisions under uncertainty and achieving a balance between exploration and exploitation.** The open source community **AI4Finance** (to efficiently automate trading) provides educational resources about deep reinforcement learning (DRL) in quantitative finance.

**To contribute?** Please check the call for contributions at the end of this page.

Feel free to report bugs using Github issues, join our mailing list: [AI4Finance](https://groups.google.com/u/1/g/ai4finance), and discuss FinRL in the slack channel:

Roadmaps of FinRL:

**FinRL 1.0**: entry-level toturials for beginners, with a demonstrative and educational purpose.

**FinRL 2.0**: intermediate-level framework for full-stack developers and professionals. Check out [ElegantRL](https://github.com/AI4Finance-LLC/ElegantRL)

FinRL provides a unified machine learning framework for various markets, SOTA DRL algorithms, benchmark finance tasks (portfolio allocation, cryptocurrency trading, high-frequency trading), live trading, etc.

## Table of Contents

- [Prior Arts](#Prior-Arts)

- [News](#News)

- [Overview](#Overview)

- [Status](#Status)

- [Installation](#Installation)

- [Docker Installation](#Docker-Installation)

- [Prerequisites](#Prerequisites)

- [Dependencies](#Dependencies)

- [Contributions](#Contributions)

- [Citing FinRL](#Citing-FinRL)

- [Call for Contributions](#Call-for-Contributions)

- [LICENSE](#LICENSE)

# Prior Arts:

We published [papers in FinTech](http://www.tensorlet.com/projects/ai-in-finance/) and now arrive at this project:

4). [FinRL](https://arxiv.org/abs/2011.09607): A Deep Reinforcement Learning Library for Automated Stock Trading in Quantitative Finance, Deep RL Workshop, NeurIPS 2020.

3). Deep Reinforcement Learning for Automated Stock Trading: An Ensemble Strategy, [paper](https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3690996) and [codes](https://github.com/AI4Finance-LLC/Deep-Reinforcement-Learning-for-Automated-Stock-Trading-Ensemble-Strategy-ICAIF-2020), ACM International Conference on AI in Finance, ICAIF 2020.

2). Multi-agent Reinforcement Learning for Liquidation Strategy Analysis, [paper](https://arxiv.org/abs/1906.11046) and [codes](https://github.com/WenhangBao/Multi-Agent-RL-for-Liquidation). Workshop on Applications and Infrastructure for Multi-Agent Learning, ICML 2019.

1). Practical Deep Reinforcement Learning Approach for Stock Trading, [paper](https://arxiv.org/abs/1811.07522) and [codes](https://github.com/AI4Finance-LLC/Deep-Reinforcement-Learning-for-Stock-Trading-DDPG-Algorithm-NIPS-2018), Workshop on Challenges and Opportunities for AI in Financial Services, NeurIPS 2018.

# News

[Towardsdatascience] [FinRL for Quantitative Finance: Tutorial for Single Stock Trading](https://towardsdatascience.com/finrl-for-quantitative-finance-tutorial-for-single-stock-trading-37d6d7c30aac)

[Towardsdatascience] [FinRL for Quantitative Finance: Tutorial for Multiple Stock Trading](https://towardsdatascience.com/finrl-for-quantitative-finance-tutorial-for-multiple-stock-trading-7b00763b7530)

[Towardsdatascience] [FinRL for Quantitative Finance: Tutorial for Portfolio Allocation](https://towardsdatascience.com/finrl-for-quantitative-finance-tutorial-for-portfolio-allocation-9b417660c7cd)

[Towardsdatascience] [Deep Reinforcement Learning for Automated Stock Trading](https://towardsdatascience.com/deep-reinforcement-learning-for-automated-stock-trading-f1dad0126a02)

[Analyticsindiamag.com] [How To Automate The Stock Market Using FinRL (Deep Reinforcement Learning Library)?](https://analyticsindiamag.com/stock-market-prediction-using-finrl/)

[量化投资与机器学习] [基于深度强化学习的股票交易策略框架(代码+文档)](https://www.mdeditor.tw/pl/p5Gg)

[运筹OR帷幄] [领读计划NO.10 | 基于深度增强学习的量化交易机器人:从AlphaGo到FinRL的演变过程](https://zhuanlan.zhihu.com/p/353557417)

[Neurohive] [FinRL: глубокое обучение с подкреплением для трейдинга](https://neurohive.io/ru/gotovye-prilozhenija/finrl-glubokoe-obuchenie-s-podkrepleniem-dlya-trejdinga/)

[ICHI.PRO] [양적 금융을위한 FinRL: 단일 주식 거래를위한 튜토리얼](https://ichi.pro/ko/yangjeog-geum-yung-eul-wihan-finrl-dan-il-jusig-geolaeleul-wihan-tyutolieol-61395882412716)

# Overview

A YouTube video about FinRL library. [YouTube] [AI4Finance Channel](https://www.youtube.com/channel/UCrVri6k3KPBa3NhapVV4K5g) for quant finance.

[ ](http://www.youtube.com/watch?v=ZSGJjtM-5jA)

](http://www.youtube.com/watch?v=ZSGJjtM-5jA)

# DRL Algorithms

We implemented Deep Q Learning (DQN), Double DQN, DDPG, A2C, SAC, PPO, TD3, GAE, MADDPG, MuZero, etc. using PyTorch and OpenAI Gym.

# Status

# DRL Algorithms

We implemented Deep Q Learning (DQN), Double DQN, DDPG, A2C, SAC, PPO, TD3, GAE, MADDPG, MuZero, etc. using PyTorch and OpenAI Gym.

# Status

Version History [click to expand]

* 2020-12-14

Upgraded to **Pytorch** with stable-baselines3; Remove tensorflow 1.0 at this moment, under development to support tensorflow 2.0

* 2020-11-27

0.1: Beta version with tensorflow 1.5

# Contributions

- FinRL is an open source library specifically designed and implemented for quant finance. Trading environments incorporating market frictions are used and provided.

- Trading tasks accompanied by hands-on tutorials with built-in DRL agents are available in a beginner-friendly and reproducible fashion using Jupyter notebook. Customization of trading time steps is feasible.

- FinRL has good scalability, with a broad range of fine-tuned state-of-the-art DRL algorithms. Adjusting the implementations to the rapid changing stock market is well supported.

- Typical use cases are selected and used to establish a benchmark for the quantitative finance community. Standard backtesting and evaluation metrics are also provided for easy and effective performance evaluation.

## Citing FinRL

```

@article{finrl2020,

author = {Liu, Xiao-Yang and Yang, Hongyang and Chen, Qian and Zhang, Runjia and Yang, Liuqing and Xiao, Bowen and Wang, Christina Dan},

journal = {Deep RL Workshop, NeurIPS 2020},

title = {FinRL: A Deep Reinforcement Learning Library for Automated Stock Trading in Quantitative Finance},

url = {https://arxiv.org/pdf/2011.09607.pdf},

year = {2020}

}

```

## Call for Contributions

Will maintain FinRL with the "AI4Finance" community and welcome your contributions!

### Contributors

Thanks to all the people who contribute.

# Contributions

- FinRL is an open source library specifically designed and implemented for quant finance. Trading environments incorporating market frictions are used and provided.

- Trading tasks accompanied by hands-on tutorials with built-in DRL agents are available in a beginner-friendly and reproducible fashion using Jupyter notebook. Customization of trading time steps is feasible.

- FinRL has good scalability, with a broad range of fine-tuned state-of-the-art DRL algorithms. Adjusting the implementations to the rapid changing stock market is well supported.

- Typical use cases are selected and used to establish a benchmark for the quantitative finance community. Standard backtesting and evaluation metrics are also provided for easy and effective performance evaluation.

## Citing FinRL

```

@article{finrl2020,

author = {Liu, Xiao-Yang and Yang, Hongyang and Chen, Qian and Zhang, Runjia and Yang, Liuqing and Xiao, Bowen and Wang, Christina Dan},

journal = {Deep RL Workshop, NeurIPS 2020},

title = {FinRL: A Deep Reinforcement Learning Library for Automated Stock Trading in Quantitative Finance},

url = {https://arxiv.org/pdf/2011.09607.pdf},

year = {2020}

}

```

## Call for Contributions

Will maintain FinRL with the "AI4Finance" community and welcome your contributions!

### Contributors

Thanks to all the people who contribute.

## Support various markets

Would like to support more asset markets, so that the users can test their stategies.

## SOTA DRL algorithms

Will continue to maintian a pool of DRL algorithms that can be treated as SOTA implementations.

## Benchmarks for typical trading tasks

To help quants have better evaluations, will maintain benchmarks for many trading tasks, upon which you can improve for your own tasks.

## Support live trading

Supporting live trading can close the simulation-reality gap, it will enable quants to switch to the real market when they are confident with their strategies.

# LICENSE

MIT

## Support various markets

Would like to support more asset markets, so that the users can test their stategies.

## SOTA DRL algorithms

Will continue to maintian a pool of DRL algorithms that can be treated as SOTA implementations.

## Benchmarks for typical trading tasks

To help quants have better evaluations, will maintain benchmarks for many trading tasks, upon which you can improve for your own tasks.

## Support live trading

Supporting live trading can close the simulation-reality gap, it will enable quants to switch to the real market when they are confident with their strategies.

# LICENSE

MIT